mathworld.wolfram.com/NormalDifferenceDistribution.html

Preview meta tags from the mathworld.wolfram.com website.

Linked Hostnames

5- 27 links tomathworld.wolfram.com

- 4 links towww.wolfram.com

- 3 links towww.wolframalpha.com

- 1 link towolframalpha.com

- 1 link towww.amazon.com

Thumbnail

Search Engine Appearance

Normal Difference Distribution -- from Wolfram MathWorld

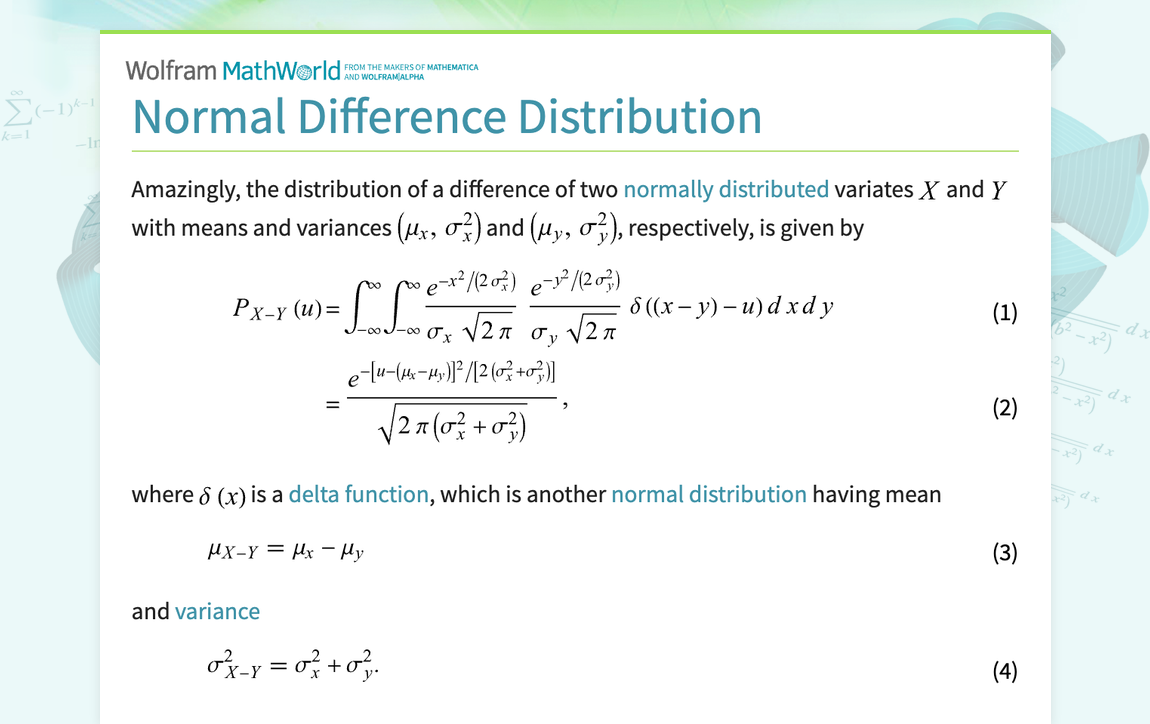

Amazingly, the distribution of a difference of two normally distributed variates X and Y with means and variances (mu_x,sigma_x^2) and (mu_y,sigma_y^2), respectively, is given by P_(X-Y)(u) = int_(-infty)^inftyint_(-infty)^infty(e^(-x^2/(2sigma_x^2)))/(sigma_xsqrt(2pi))(e^(-y^2/(2sigma_y^2)))/(sigma_ysqrt(2pi))delta((x-y)-u)dxdy (1) = (e^(-[u-(mu_x-mu_y)]^2/[2(sigma_x^2+sigma_y^2)]))/(sqrt(2pi(sigma_x^2+sigma_y^2))), (2) where delta(x) is a delta function, which is another normal...

Bing

Normal Difference Distribution -- from Wolfram MathWorld

Amazingly, the distribution of a difference of two normally distributed variates X and Y with means and variances (mu_x,sigma_x^2) and (mu_y,sigma_y^2), respectively, is given by P_(X-Y)(u) = int_(-infty)^inftyint_(-infty)^infty(e^(-x^2/(2sigma_x^2)))/(sigma_xsqrt(2pi))(e^(-y^2/(2sigma_y^2)))/(sigma_ysqrt(2pi))delta((x-y)-u)dxdy (1) = (e^(-[u-(mu_x-mu_y)]^2/[2(sigma_x^2+sigma_y^2)]))/(sqrt(2pi(sigma_x^2+sigma_y^2))), (2) where delta(x) is a delta function, which is another normal...

DuckDuckGo

Normal Difference Distribution -- from Wolfram MathWorld

Amazingly, the distribution of a difference of two normally distributed variates X and Y with means and variances (mu_x,sigma_x^2) and (mu_y,sigma_y^2), respectively, is given by P_(X-Y)(u) = int_(-infty)^inftyint_(-infty)^infty(e^(-x^2/(2sigma_x^2)))/(sigma_xsqrt(2pi))(e^(-y^2/(2sigma_y^2)))/(sigma_ysqrt(2pi))delta((x-y)-u)dxdy (1) = (e^(-[u-(mu_x-mu_y)]^2/[2(sigma_x^2+sigma_y^2)]))/(sqrt(2pi(sigma_x^2+sigma_y^2))), (2) where delta(x) is a delta function, which is another normal...

General Meta Tags

21- titleNormal Difference Distribution -- from Wolfram MathWorld

- DC.TitleNormal Difference Distribution

- DC.CreatorWeisstein, Eric W.

- DC.DescriptionAmazingly, the distribution of a difference of two normally distributed variates X and Y with means and variances (mu_x,sigma_x^2) and (mu_y,sigma_y^2), respectively, is given by P_(X-Y)(u) = int_(-infty)^inftyint_(-infty)^infty(e^(-x^2/(2sigma_x^2)))/(sigma_xsqrt(2pi))(e^(-y^2/(2sigma_y^2)))/(sigma_ysqrt(2pi))delta((x-y)-u)dxdy (1) = (e^(-[u-(mu_x-mu_y)]^2/[2(sigma_x^2+sigma_y^2)]))/(sqrt(2pi(sigma_x^2+sigma_y^2))), (2) where delta(x) is a delta function, which is another normal...

- descriptionAmazingly, the distribution of a difference of two normally distributed variates X and Y with means and variances (mu_x,sigma_x^2) and (mu_y,sigma_y^2), respectively, is given by P_(X-Y)(u) = int_(-infty)^inftyint_(-infty)^infty(e^(-x^2/(2sigma_x^2)))/(sigma_xsqrt(2pi))(e^(-y^2/(2sigma_y^2)))/(sigma_ysqrt(2pi))delta((x-y)-u)dxdy (1) = (e^(-[u-(mu_x-mu_y)]^2/[2(sigma_x^2+sigma_y^2)]))/(sqrt(2pi(sigma_x^2+sigma_y^2))), (2) where delta(x) is a delta function, which is another normal...

Open Graph Meta Tags

5- og:imagehttps://mathworld.wolfram.com/images/socialmedia/share/ogimage_NormalDifferenceDistribution.png

- og:urlhttps://mathworld.wolfram.com/NormalDifferenceDistribution.html

- og:typewebsite

- og:titleNormal Difference Distribution -- from Wolfram MathWorld

- og:descriptionAmazingly, the distribution of a difference of two normally distributed variates X and Y with means and variances (mu_x,sigma_x^2) and (mu_y,sigma_y^2), respectively, is given by P_(X-Y)(u) = int_(-infty)^inftyint_(-infty)^infty(e^(-x^2/(2sigma_x^2)))/(sigma_xsqrt(2pi))(e^(-y^2/(2sigma_y^2)))/(sigma_ysqrt(2pi))delta((x-y)-u)dxdy (1) = (e^(-[u-(mu_x-mu_y)]^2/[2(sigma_x^2+sigma_y^2)]))/(sqrt(2pi(sigma_x^2+sigma_y^2))), (2) where delta(x) is a delta function, which is another normal...

Twitter Meta Tags

5- twitter:cardsummary_large_image

- twitter:site@WolframResearch

- twitter:titleNormal Difference Distribution -- from Wolfram MathWorld

- twitter:descriptionAmazingly, the distribution of a difference of two normally distributed variates X and Y with means and variances (mu_x,sigma_x^2) and (mu_y,sigma_y^2), respectively, is given by P_(X-Y)(u) = int_(-infty)^inftyint_(-infty)^infty(e^(-x^2/(2sigma_x^2)))/(sigma_xsqrt(2pi))(e^(-y^2/(2sigma_y^2)))/(sigma_ysqrt(2pi))delta((x-y)-u)dxdy (1) = (e^(-[u-(mu_x-mu_y)]^2/[2(sigma_x^2+sigma_y^2)]))/(sqrt(2pi(sigma_x^2+sigma_y^2))), (2) where delta(x) is a delta function, which is another normal...

- twitter:image:srchttps://mathworld.wolfram.com/images/socialmedia/share/ogimage_NormalDifferenceDistribution.png

Link Tags

4- canonicalhttps://mathworld.wolfram.com/NormalDifferenceDistribution.html

- preload//www.wolframcdn.com/fonts/source-sans-pro/1.0/global.css

- stylesheet/css/styles.css

- stylesheet/common/js/c2c/1.0/WolframC2CGui.css.en

Links

36- http://www.wolframalpha.com/input/?i=beta+distribution

- http://www.wolframalpha.com/input/?i=bivariate+normal+distribution

- http://www.wolframalpha.com/input/?i=continuous+distributions

- https://mathworld.wolfram.com

- https://mathworld.wolfram.com/DeltaFunction.html